DeFi Wallet to Bank Account Bridge | Scroll Wallet

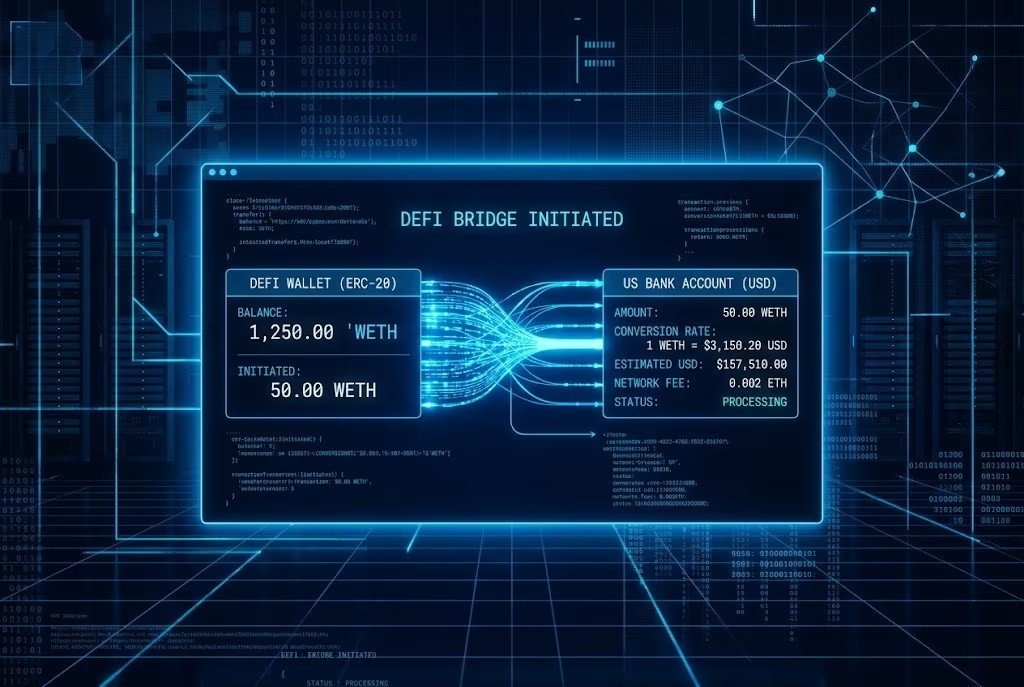

You can move crypto to a US bank account in minutes using stablecoins and modern payout rails. The source flow starts with a crypto-to-stablecoin conversion and then sends funds through ACH, card, or other supported banking channels with compliance checks attached.

Compare key payout rails for crypto-to-fiat withdrawals in the US. ACH is usually low cost, SWIFT supports international bank movement, and card rails can be faster but more expensive.

| Rail | Speed | Cost | Limits |

|---|---|---|---|

| ACH | Same-day to 2 days | $0.20-$1.50 | Up to $1M per transaction |

| SWIFT | 1-6 days | $15+ | Varies by platform |

| SEPA | N/A (Europe only) | N/A | Not applicable to US domestic withdrawals |

| Visa Direct | Seconds to minutes | 1-2% + flat fee | About $10K daily |

Source of data: BVNK payment-rail comparison.

The source positions 2024-2026 as a rapid expansion period for crypto-to-bank settlement in the US. It highlights stablecoin usage growth, stronger institutional participation, and broader pressure for faster global payout rails.

Market commentary in the article links institutional adoption to treasury and settlement workflows, where stablecoins are used to reduce transfer friction compared with legacy-only paths. For additional trend context, see the Payments Association trends report.

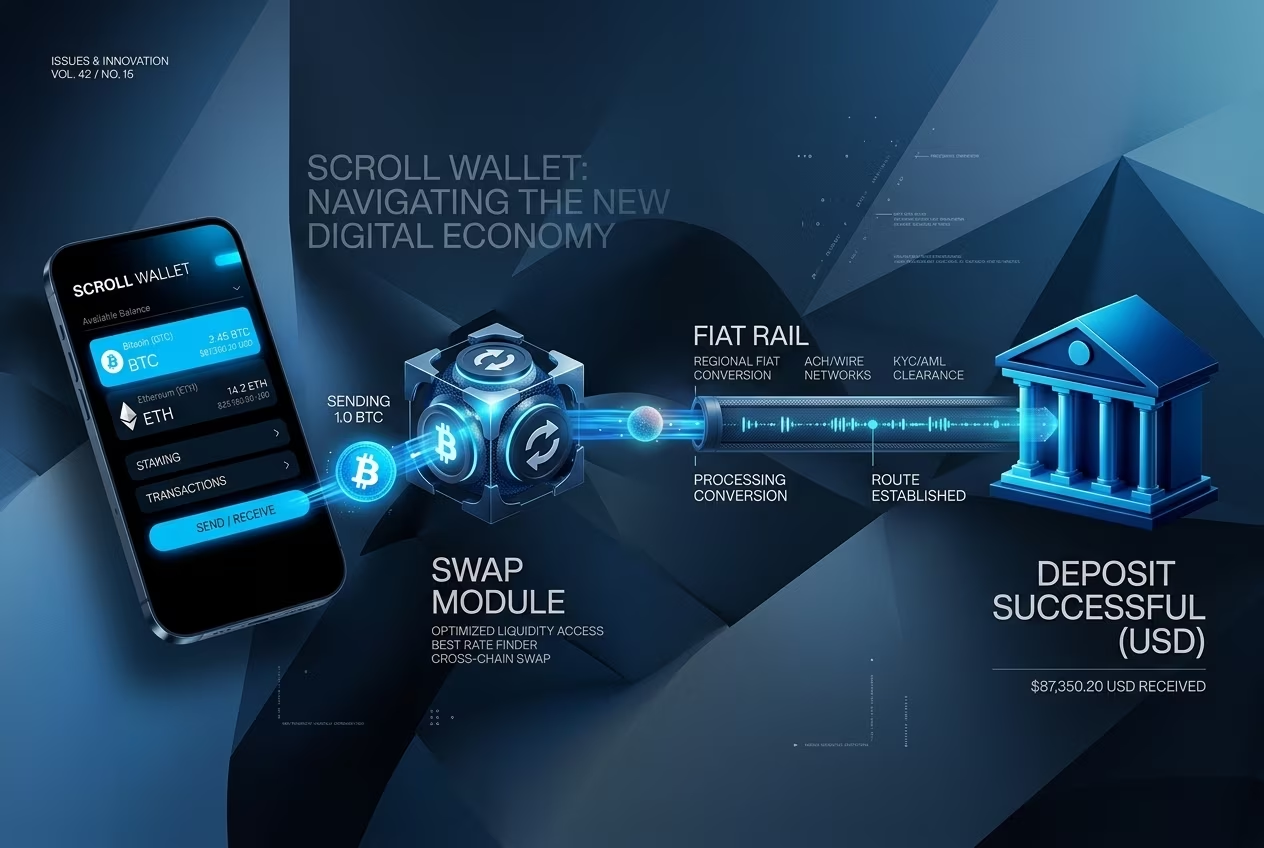

Operationally, the article frames Scroll Wallet as an execution layer for multi-chain transfers with user-side custody and lower route complexity. For adjacent architecture context, compare with What Is Scroll Network Wallet? Secure L2 Solution 2026 | Scroll Wallet.

The source favors low-fee assets for bank withdrawal preparation, with Litecoin highlighted for cost and confirmation speed. It contrasts LTC costs against higher, congestion-sensitive BTC and ETH routes.

Reference discussion uses daily cashout examples and compares transfer behavior before fiat off-ramp completion. For fee-focused context, see Margex fee benchmark commentary.

The article still includes BTC, ETH, and stablecoin pathways, but recommends choosing assets based on route economics and settlement urgency rather than ticker preference alone.

Follow these steps in Scroll Wallet to withdraw crypto to a bank account with lower operational risk.

Source estimates place total crypto-to-bank costs in a 0.5%-2% range when combining network fees, exchange spread, and fiat conversion spread. ACH can be low or free at platform level, while wire routes often add fixed banking charges.

| Fee Type | Typical Cost |

|---|---|

| On-chain (BTC) | 0.0005 BTC (~$30-$50) |

| On-chain (ETH) | $5-$20 |

| On-chain (USDC) | <$1 |

| Exchange fees | 0-0.6% + network/gas |

| Fiat spreads | 0.3-1.2% |

| Total crypto-to-bank | 0.5-2% |

| Wire transfer (US bank) | $10-$25 |

| ACH transfer | Often free (slower) |

Source of data: StormGain fee analysis.

The source frames Travel Rule compliance as a core requirement for larger crypto-to-bank transfers in US-facing flows. It highlights identity-data capture obligations at higher transfer thresholds and ongoing AML/SAR responsibilities for suspicious activity.

For reference, review FinCEN travel-rule advisory material and current FinCEN registration guidance.

Practical implication for users: expect verification at payout touchpoints, keep documentation consistent, and review transfer previews carefully before submission.

The source describes frequent user complaints around payout delays, account freezes, fraud, and verification friction. It also highlights phishing and fake-service risk when users leave verified wallet flows.

In this model, major failure points include incorrect recipient data, unverified off-ramp partners, and rushed approvals in volatile markets. Defensive baseline includes 2FA, address whitelists, test-size transfers, and strict provider verification.

For a broader self-custody security baseline, compare with Browser Cryptowallet Security Risks Solved In 2026 | Scroll Wallet.

Source positioning emphasizes fast route execution, non-custodial key ownership, and low-fee multi-chain operation in Scroll Wallet. It presents this as a way to reduce payout friction under fragmented Layer-2 and bridge-heavy conditions.

Execution benefits in the source include lower fee overhead, transparent transaction checks, and easier route handling across supported networks. For deeper product context, see What Is Scroll Network Wallet? Secure L2 Solution 2026 | Scroll Wallet.

Even with better tooling, users still need manual discipline: verify bridge URLs, verify token contracts, and track confirmations in block explorers before treating a payout as final.

Crypto-to-bank transfers are moving toward faster, lower-friction rails, but security and compliance checks remain mandatory. The source positions Scroll Wallet as a practical self-custody layer for handling this shift.

For daily operations, keep a repeatable workflow: convert through trusted routes, confirm recipient details, and monitor transfer state until final settlement.

Recommended controls:

For full setup and product overview, visit the Scroll Wallet homepage.